Why This Matters to Buyers and Investors

On 13 May 2025, the Bank of England reduced its base interest rate from 4.5% to 4.25%, its first cut since mid-2023. While modest, this decision reflects growing concerns about economic slowdown and declining wage growth.

For anyone considering buying property in the UK, especially in London, this change affects more than just macroeconomics. It shapes how affordable mortgages are, how attractive rental yields become, and how likely the market is to stabilise or grow.

Caution from the Bank of England: This Is Not 2009

The BoE is clear: this is not a return to ultra-low rates. Future decisions will be data-driven and closely tied to inflation performance. In fact, the Monetary Policy Committee was split, with 5 members voting to cut and 4 voting to hold, highlighting the cautious stance within the Bank.

Governor Andrew Bailey reiterated that the priority remains achieving the 2% inflation target sustainably. Investors should view this as a supportive but temporary window, rather than a long-term trend.

What to Expect Next: June Meeting and Beyond

At its 18 June 2025 meeting, the Bank of England’s Monetary Policy Committee (MPC) voted 6–3 to hold rates at 4.25%, pushing the next decision to 7 August. While inflation remains elevated at 3.4% in May, the Bank prioritised caution amid global instability, rising oil prices, Middle East tensions, and trade-policy uncertainties.

Governor Andrew Bailey emphasised that although the Bank views rates as on a “gradual downward path”, future cuts depend on clear signs of wage and price pressures easing. Notably, three MPC members voted for a further cut, suggesting easing could begin in August, followed by additional cuts later this year, possibly reaching 3.75% by December.

Key factors to monitor heading into the summer and autumn:

- Labour market: Weakening employment and slowing wage trends.

- Inflation trajectory: Crude oil and regulated cost pressures may keep inflation above target.

- Global uncertainties: Conflicts and tariffs may delay monetary easing.

Practical takeaway for buyers:

This pause at 4.25% maintains current mortgage affordability, and potential further savings may emerge with cuts in August, but if inflation or geopolitics worsen, the Bank could delay. So, if you’re planning to enter the market, consider fixing a deal now or arranging in advance, while monitoring August signals.

Economic Signals Behind the Rate Cut

- Unemployment has risen to 4.5%, the highest since 2021.

- Wage growth is slowing: 5.6% in Q1 2025, down from over 6% in late 2024.

- Inflation is easing, with CPI recorded at 3.4% in May 2025, and expected to fluctuate around 3.5–3.7% through the summer, despite persistent energy-related pressures.

These figures suggest that household budgets are tightening, and the UK economy is entering a cautious phase. The Bank of England’s decision aims to protect demand without reigniting inflation.

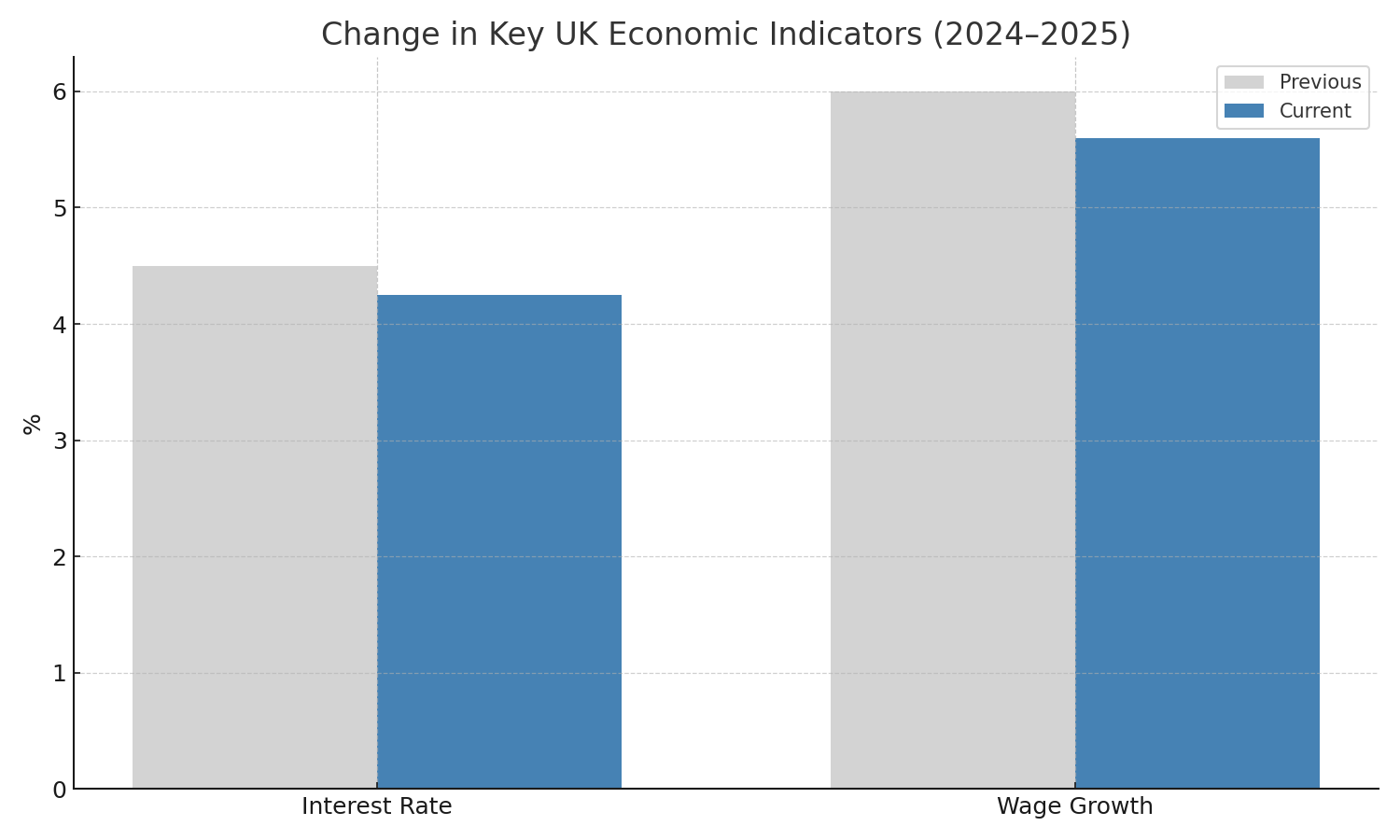

Visual Snapshot: How Rates and Wages Have Shifted

The chart below compares the interest rate and wage growth in late 2024 vs early 2025. These shifts highlight why the Bank of England decided to ease monetary conditions.

How the Rate Cut Affects Different Types of Property Buyers in London

While the interest rate cut benefits the market overall, its impact differs depending on who you are.

First-time buyers may find it easier to step onto the ladder, while investors might see improved leverage. Meanwhile, international buyers could face unique advantages in currency and financing access.

Here’s how different buyer groups stand to gain, or reposition, their strategies in light of this change.

Summary Table

First-Time Buyers: How Affordability Improves

Lower interest rates offer immediate relief to first-time buyers, who often face the toughest financial barriers in the UK housing market, especially in London. While the base rate cut reduces borrowing costs, significant challenges remain, most notably the high upfront deposit requirements.

In London, the average deposit needed for an entry-level property can exceed £150,000, putting homeownership out of reach for many without family support or long-term savings. However, the recent rate cut by the Bank of England has led lenders to lower their fixed-rate offers. Notably, two-year fixed mortgage deals with 60% loan-to-value (LTV) are now available at approximately 3.99%, making repayment terms more accessible.

To illustrate the impact: a standard £400,000 mortgage at 80% LTV would now cost about £70 less per month under a 4.25% rate compared to the previous 4.5%. While this may appear modest, such savings accumulate over time and ease the monthly financial pressure, a crucial factor for younger or lower-income buyers trying to secure their first home.

Importantly, the UK government’s Mortgage Guarantee Scheme, set to restart in July 2025, is expected to further enhance affordability. It allows eligible first-time buyers to purchase homes up to £600,000 with just a 5% deposit, backed by a government guarantee to lenders. When combined with falling interest rates, this scheme significantly lowers the barriers to entry and may trigger a rise in first-time buyer activity in the latter half of the year.

Looking for affordable new-build homes?Explore verified developments across London with low entry prices and flexible mortgage options.View First-Time Buyer-Friendly Listings on Entralon

Buy-to-Let Investors: Boosting Yields Through Leverage

The recent interest rate cut is significant for buy-to-let investors, who rely on leveraged financing to amplify their rental income returns. Even a modest drop in mortgage rates can enhance profitability across a rental portfolio.

As of February 2025, the average interest rate for two-year fixed buy-to-let mortgages (at 75% loan-to-value) has declined to approximately 4.3%. This shift improves cash flow for landlords, especially those renewing expiring deals or acquiring new properties under more favourable lending conditions.

On the rental income side, returns remain robust. According to Nationwide QA, average buy-to-let yields across the UK reached 7.4% in Q1 2025, with some regions, particularly the North East, offering returns as high as 9.2%. In London, where property values are higher, gross yields typically range between 5.5% and 5.7%. While these yields are lower than in regional hotspots, London’s strong rental demand and capital stability continue to attract long-term investors.

The combination of declining borrowing costs (~4.3%) and steady rental yields (~5.7%) ensures that net returns remain attractive, especially for investors leveraging mortgage finance. With interest costs decreasing, the spread between mortgage rates and rental yields widens, enhancing the investor’s real return after financing.

Example: Consider a property purchased for £450,000 and rented at £1,800/month. Under current market conditions, this scenario delivers an estimated net ROI of ~4.8%, accounting for mortgage payments and typical operating costs. This figure reflects the healthier margins made possible by today’s lending environment and the resilience of London’s rental market.

How the Rate Cut Helps Expats and International Buyers

For expatriates and relocating professionals, especially those planning to live and work in London, the Bank of England’s rate cut opens up new financial opportunities that go beyond simple interest savings.

One of the most immediate advantages is improved access to mortgages, driven by heightened lender competition. As base rates decline, many banks and mortgage providers begin offering more attractive deals, not only for UK residents but also for non-resident applicants.

This is particularly relevant to skilled professionals relocating from abroad, who may previously have faced stricter lending criteria or higher interest margins.

Additionally, the slightly weaker pound means that international buyers can currently benefit from favourable currency exchange rates, effectively increasing their purchasing power when converting savings from USD, EUR, AED, or other currencies into GBP.

To meet growing demand, an increasing number of lenders have rolled out bespoke mortgage products for non-residents. These often include fixed-rate packages with clearer eligibility and documentation pathways, especially appealing for professionals who have secured employment in the UK and need to settle quickly.

For example, some lenders now accept income verification from international employers, provide longer decision windows, or offer hybrid repayment models tailored to relocation scenarios.

Final Thoughts

The Bank of England’s rate cut to 4.25% offers a window of opportunity, but not a long-term shift in policy. With inflation still a concern and the next MPC decision around the corner, this moment may represent a short-lived advantage for buyers looking to enter the London market.

If you’ve been waiting for the right conditions, better mortgage deals, improved affordability, or enhanced investment margins, this could be your signal to act. But timing and strategy matter.

At Entralon, we combine trusted data, full-market listings, and tailored insights to help you find the right property that aligns with your goals, lifestyle, and long-term vision.

Speak to us today for a personalised plan, whether you’re a first-time buyer, investor, or international buyer.

View All Verified London Listings

FAQs

Q: Will mortgage rates in the UK drop further after this cut?

A: Lenders may gradually adjust rates, but much depends on inflation data. Don’t expect dramatic drops; focus on stability.

Q: How does a lower base rate affect buy-to-let investors?

A: It reduces borrowing costs and improves net yields. However, rental demand and property type still matter more.

Q: Is now a good time for expats to invest in London?

A: With softened interest rates and strong rental demand, yes, especially in high-growth suburban zones.

Discussion