For years, housing costs were explained by demand, supply, and interest rates. Yet a different force has been tightening its grip on real-estate economics reinsurance.

When the price of global risk protection rises, that increase ripples through insurers, property owners, and eventually tenants. The cost of rent in Miami or Denver can now be influenced by a catastrophe halfway across the world.

This isn’t just a story of climate volatility. It’s a financial transmission chain linking the capital markets that fund insurers to the cash flows that sustain multifamily properties.

The problem is simple but profound: global reinsurance price shocks are distorting local housing markets, compressing margins, and challenging traditional models of property valuation. The solution will require finance itself to evolve, to design new ways of insulating real assets from systemic insurance volatility.

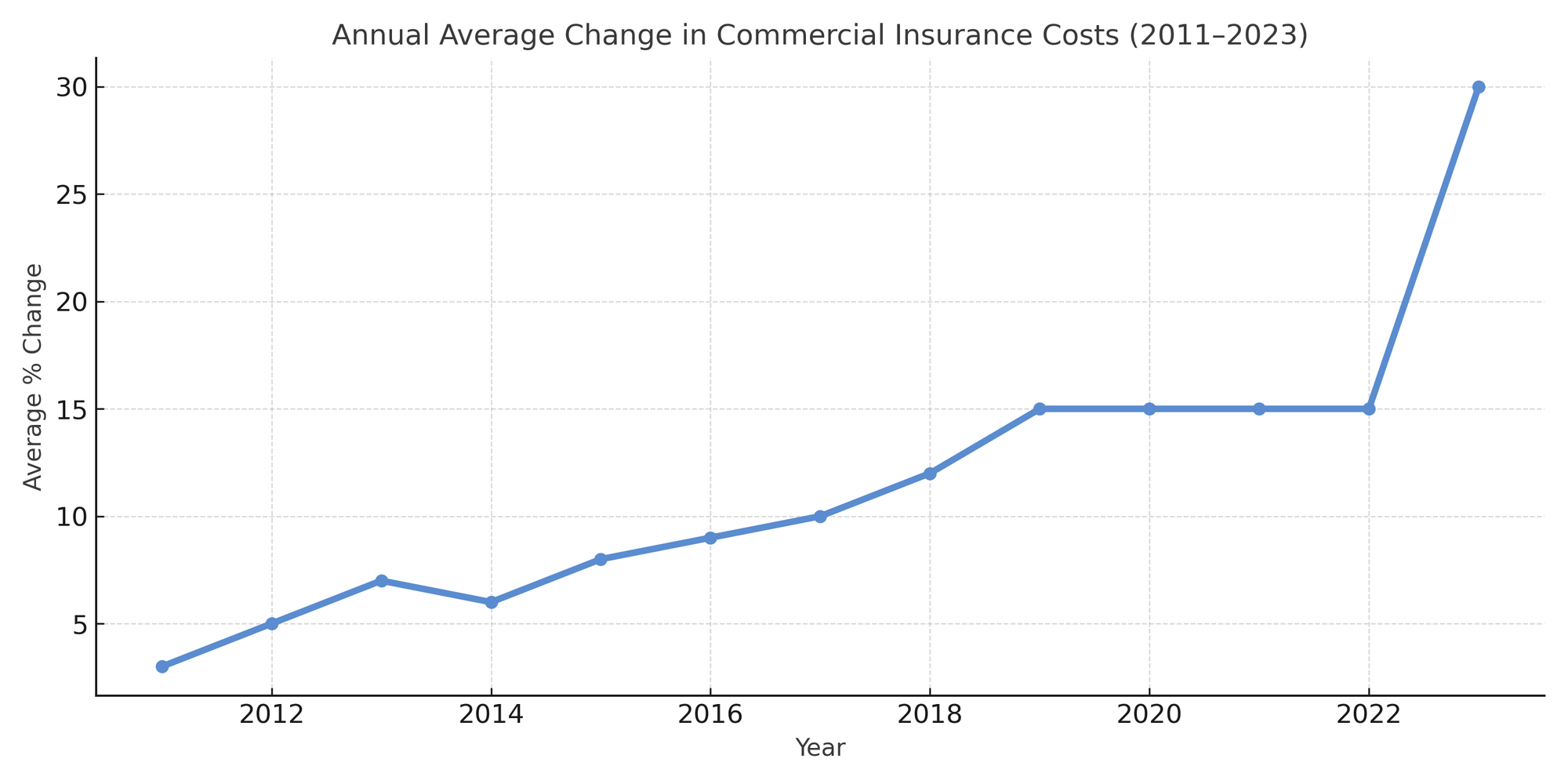

Over the past decade, insurance costs for commercial and multifamily properties across the United States have risen sharply, with especially steep increases since 2019. In some regions, the annual rise has exceeded 15 percent year after year, culminating in nearly 30 percent during 2023.

Three structural forces explain this surge. First, insurers are recalibrating premiums to reflect localized climate and disaster risk, incorporating forward-looking data from national risk indices. Second, the cost of reinsurance, the market where insurers themselves buy protection, has climbed steeply since 2018, particularly in hurricane-exposed states such as Florida, Texas, and Louisiana. Third, insurers are spreading the impact of losses from one region to others, raising premiums even in lower-risk states to maintain solvency after severe events elsewhere.

Insurance costs for commercial properties climbed steadily since 2011, surging nearly 30% by 2023.

For financial institutions, these dynamics blur the line between local property performance and global financial stress. Rising insurance expenses reduce net operating income, erode collateral values, and tighten credit conditions. In a market where as much as two-thirds of insurance costs are passed through to rent, affordability declines while underwriting risk increases.

In effect, the price of risk, once confined to the insurance sector, has become a macroeconomic factor shaping every level of real-estate finance.

Join Entralon Hub

Receive weekly research-backed articles that turn complex property data into clear, actionable intelligence.

No spam. Unsubscribe anytime.

The Hidden Dynamic Behind the Problem

The underlying issue is conceptual. Most financial actors still treat insurance as a fixed operating cost, a line item rather than a signal. In reality, the insurance and reinsurance markets have evolved into a parallel risk-pricing system that directly influences asset performance.

As climate-related disasters intensify, reinsurers price risk through a global lens. When those prices rise, insurers adjust their models, passing costs down to property owners who often have little ability to offset them.

The effect is not confined to coastal or high-risk areas; it’s systemic. Losses in one region, like Louisiana’s hurricane season, can trigger higher premiums for apartment complexes in Colorado.

Recognizing this shift requires a change in perspective: reinsurance is no longer a background cost but a macro-financial variable. It links physical risk, capital markets, and social outcomes in a continuous feedback loop. For lenders, investors, and asset managers, ignoring that linkage means missing a key driver of future cash flows and valuation risk.

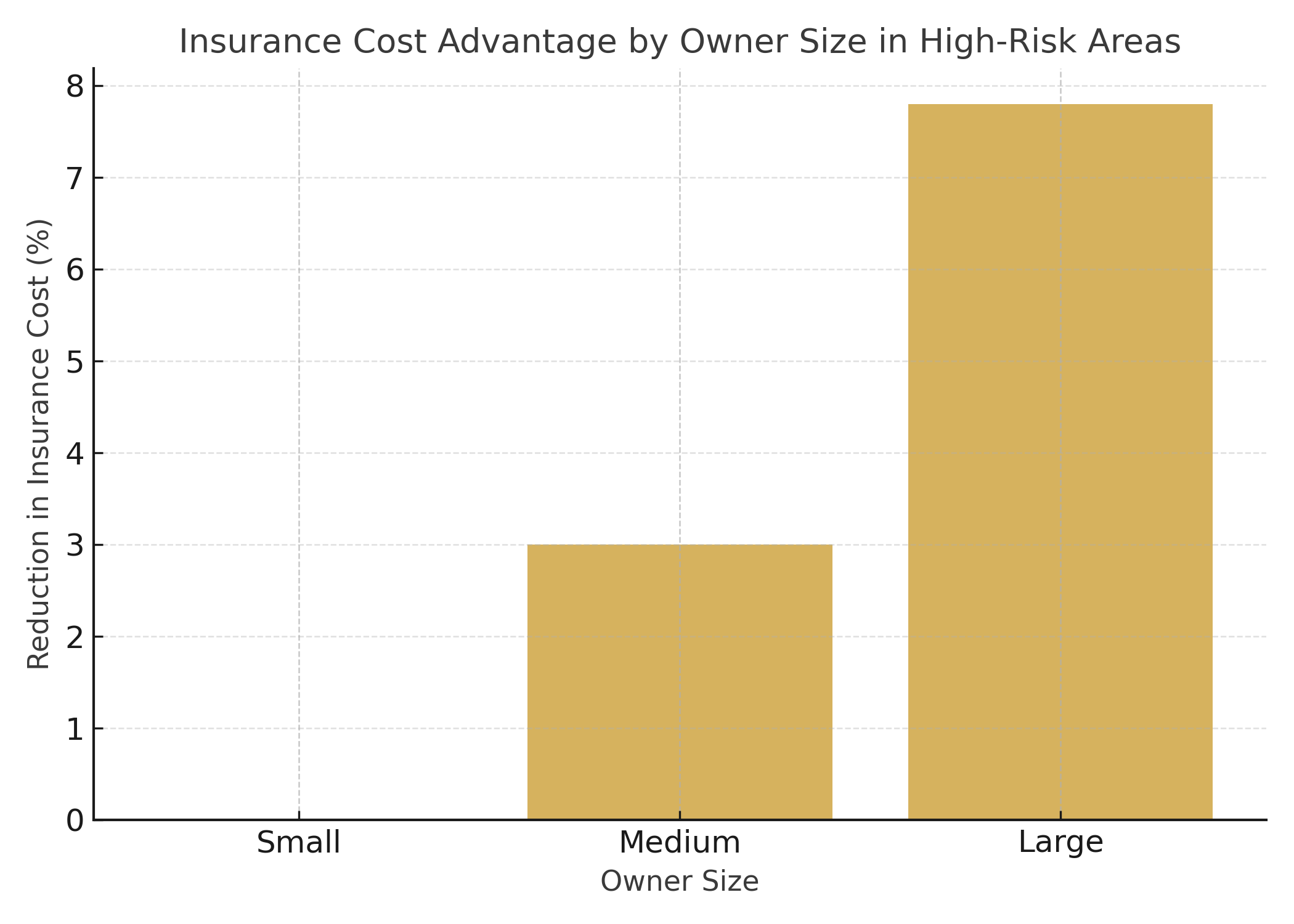

Large property owners in high-risk areas enjoy up to 7.8% lower insurance costs.

From Insight to Action

To manage this new landscape, financial institutions must translate awareness into strategy. The goal is not to eliminate risk, that’s impossible, but to anticipate and absorb it through informed design and collaboration.

Step 1: Rebuild Risk Models Around Insurance Costs

Integrate projected insurance and reinsurance trends into every asset and credit model. Historical averages no longer hold. A 10 percent change in insurance expense can now cut net income far more than interest-rate fluctuations. Embedding these variables into stress tests provides early visibility into margin compression and loan exposure.

Free membership in the global think tank shaping the future of real estate.

Wirginia Leszczyńska is COO & CSO at DL Invest Group, driving 17+ years of strategic growth, digital transformation, and ESG-led investment to maximize portfolio value in Poland’s property market.

Logan is an MIT graduate with 5 years of experience in RE finance and development. At Boyer and PEG, he managed major industrial projects and secured institutional capital. He holds a BS from BYU.

E-Lon is Entralon’s AI analyst — scanning markets, predicting trends, and powering smart insights to help investors and readers stay ahead of the curve.

Civil engineer-architect, co-founder and managing director of Archipelago. Specialised in research-driven architecture for living, care, work and learning, with a focus on user experience, sustainability and circular building economics.

Karsten R. Gerdrup is Director of Analysis at Norges Bank, specializing in monetary policy, macro-financial modeling, and forecasting. An economist with extensive policy experience, he contributes to financial stability and fiscal policy analysis.

Dr Farid Zadeh Bagheri is an entrepreneur and strategist focused on redefining access in real estate through structural insight, technology, and global investment experience.

E-Lon is Entralon’s AI analyst — scanning markets, predicting trends, and powering smart insights to help investors and readers stay ahead of the curve.

Subscribe to Newsletter

Join me on this exciting journey as we explore the boundless world of web design together.