2025 is not about speculation; it’s about informed, strategic investing.

As the global property market adapts to shifting economic conditions and evolving buyer sentiment, two cities are commanding investor focus in the new-build real estate segment: Dubai, the rapidly accelerating off-plan market driven by global demand, and London, the historically stable safe haven offering transparency and regulated growth.

If you’re evaluating new-build property investment, whether for rental income, visa eligibility, or long-term capital appreciation, this data-backed comparison helps you make a well-aligned decision. We examine five core dimensions: price trends, construction pipelines, buyer demand, investment returns, and economic resilience.

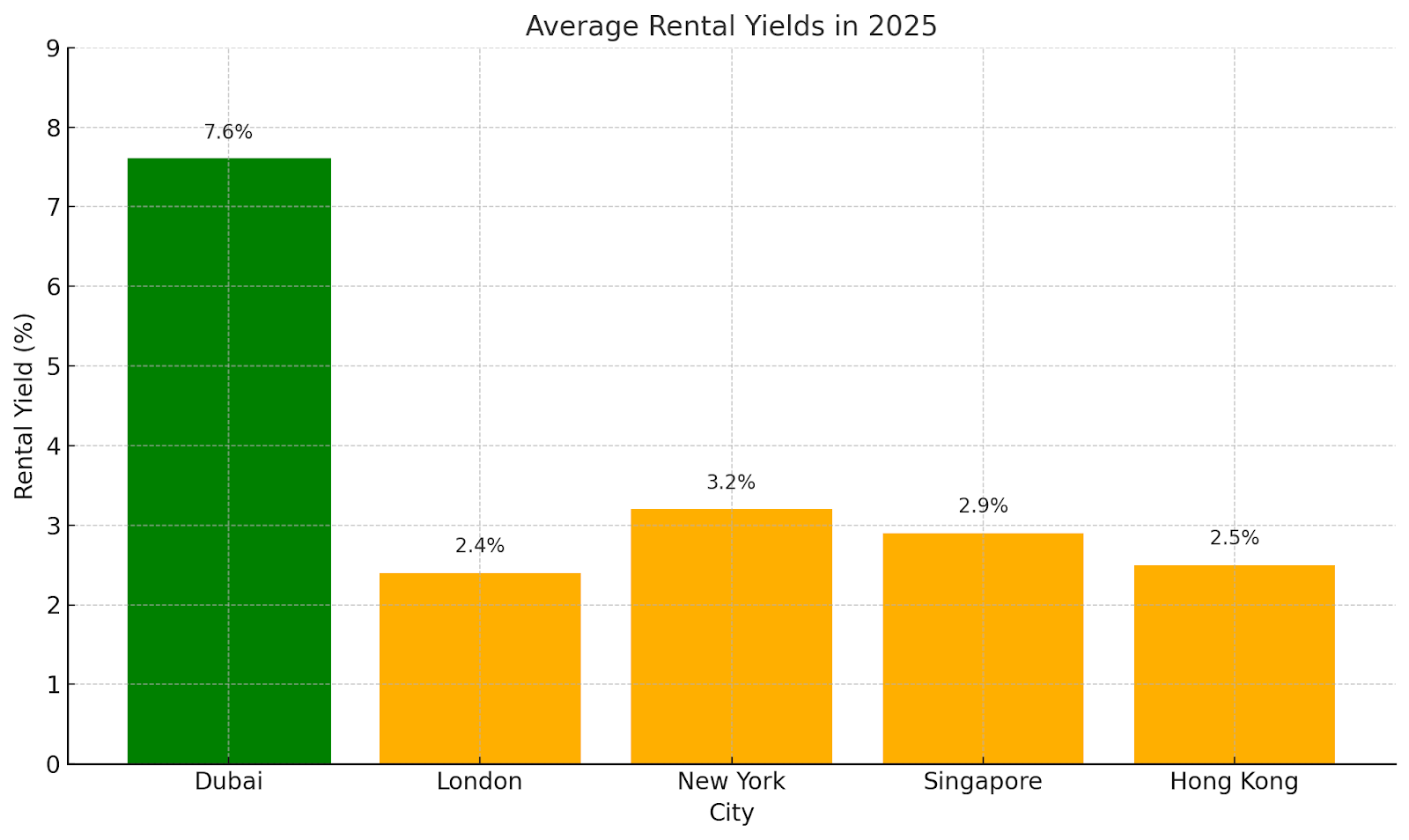

The numbers are clear. Dubai leads with 19% annual price growth, 7.6% average yields, and surging investor interest, thanks to programs like the UAE Golden Visa. Key districts such as Jumeirah Village Circle (JVC) and Dubai South account for over 59% of all off-plan transactions, fuelling a highly active sales pipeline.

London, by contrast, continues to attract first-time buyers and global investors, comprising 13% of transactions. While price growth is modest (~2%) and construction faces constraints, the city offers EPC A/B-rated inventory, strong governance, and long-term structural demand.

These are two different propositions:

- Dubai offers speed, yield, and entry momentum.

- London offers stability, regulation, and security over time.

The right choice depends on your timeline, goals, and appetite for risk.

Want to compare the full spectrum of new-build opportunities in Dubai and London?

Let Entralon guide your journey with verified listings, AI-powered insight, and commission-free, buyer-aligned support, from search to post-purchase.

Dubai Real Estate Market in 2025: The Rise of Off-Plan Powerhouses

Market Performance: Explosive Growth Fueled by Off-Plan Sales

Dubai’s new build property market is leading the global stage in 2025, driven by exceptional off-plan performance. According to REIDIN, apartment prices in November 2024 soared 19.4% year-over-year, the highest growth rate among global cities. By December, the average apartment price reached AED 1.4 million (~£294,000), reflecting a sharp rise in both freehold and leasehold districts.

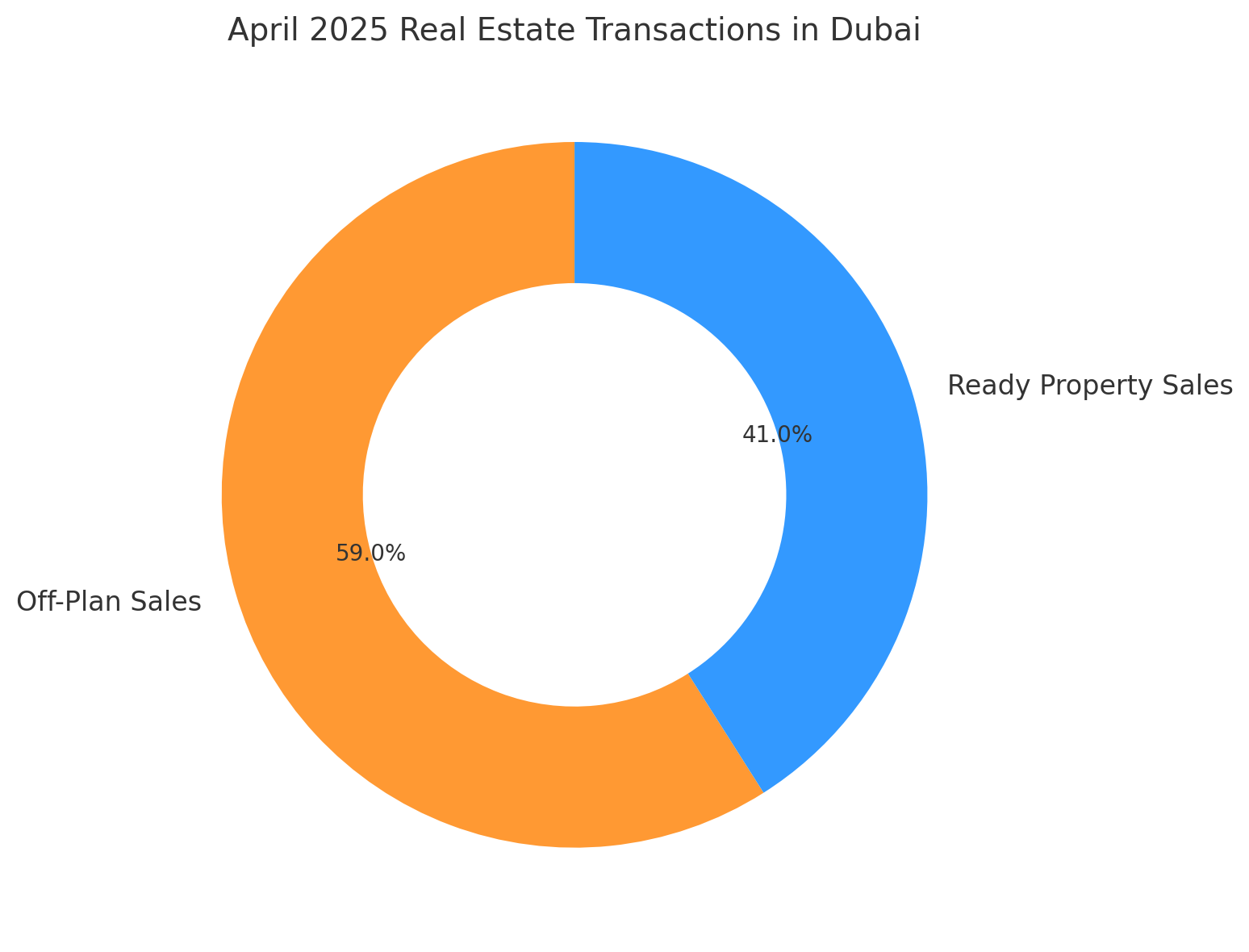

Off-plan sales are dominating the landscape, accounting for 59% of all property transactions in April 2025, based on data from the Dubai Land Department. Meanwhile, average rental yields across the city have surpassed 7.6%, with top-performing areas, such as Jumeirah Village Circle (JVC) and Dubai Marina, offering even higher returns. For global investors, this makes Dubai a prime choice for short-to-mid-term capital growth and income-generating property investment.

Supply Pipeline: Ambitious, But Facing Delays

Dubai’s construction pipeline remains vast and forward-looking. As per Cavendish Maxwell, over 76,000 new residential units are expected to be completed in 2025, with a projected total of 243,000 units by 2027. Strategic development zones like JVC and Dubai South continue to attract both local and international developers.

However, the market is not without its friction points. Despite the optimistic pipeline, only 21,507 apartments were completed during the first nine months of 2024, according to ValuStrat. Construction delays, caused by global supply chain disruptions, labour shortages, and rising raw material costs, have slowed delivery in several large-scale projects.

Demand Drivers: Golden Visas and Expat Surge

Dubai’s real estate boom is underpinned by a potent mix of demographic growth and investor-friendly visa reforms. With the population currently at 3.92 million and projected to exceed 4 million by 2026, residential demand continues to rise. The UAE Golden Visa has already attracted more than 100,000 high-net-worth individuals, many of whom have chosen real estate as their preferred asset class.

Strong capital inflows from India, China, and the UK reflect Dubai’s appeal to global buyers. Factors such as 0% property tax, a favourable exchange rate, and a stable legal framework continue to reinforce Dubai’s image as a safe and lucrative investment environment. Moreover, rising rental prices, up 10% YoY, are pushing residents toward off-plan purchases as a more affordable and future-proof path to ownership.

Innovation & Sustainability: Branded & Green Living

Dubai is reshaping its urban identity through a bold commitment to innovation and luxury. The city now leads the world in branded residences, with over 140 developments in the pipeline, outpacing even London and New York, according to Savills.

Equally notable is the shift toward green-certified buildings. Approximately 35% of all new build projects in Dubai are now LEED-certified, with developers integrating smart home technologies, energy-efficient materials, and ESG-aligned design principles. For international buyers, particularly those from Europe and North America, these features are not only appealing, they’re expected.

Economic Context: Diversified & Resilient

Dubai’s economic foundation remains a key pillar of real estate confidence. According to the UAE Central Bank, the country’s GDP is projected to grow by 4.5% in 2025, fueled largely by non-oil sectors like tourism, fintech, logistics, and renewable energy, which now contribute over 14.4% to national GDP.

The removal of the UAE from the FATF Grey List in 2024 has boosted international credibility, encouraging cross-border investments and institutional interest. While regional geopolitical risks persist, Dubai’s economic diversification and strong governance structure provide a robust safety net for investors looking for both security and upside.

Conclusion for Investors:

Dubai is not just outperforming global peers; it’s redefining what a high-growth, investor-friendly property market looks like in 2025. Whether you’re targeting rental income, a passport-linked investment, or a high-yield off-plan opportunity, Dubai’s new build sector is one of the most dynamic places to watch.

Ready to explore the most promising off-plan and new build properties in Dubai, backed by real data and buyer-first insight?

Let Entralon guide your next move.

London New Build Market in 2025: Steady Resilience or Structural Challenge?

Market Performance: Modest Growth Amid Affordability Barriers

London’s new build property market is treading cautiously in 2025, shaped by rising affordability pressures, shifting tax policies, and muted buyer sentiment. According to Knight Frank, average new build prices rose by 2% year-on-year in Q3 2024 and are forecast to continue at this modest pace throughout 2025.

However, price trends are uneven. Nationwide reported a 0.8% monthly price drop in June 2025, the sharpest since 2022, largely driven by stamp duty threshold cuts, inflation fatigue, and tighter household budgets. With average new build apartment prices reaching £590,000 as of December 2024 (per CBRE), affordability challenges are mounting, particularly for first-time buyers facing stagnant wage growth, high rental inflation, and rising energy costs.

Supply Shortages: Planning Headaches and High Costs

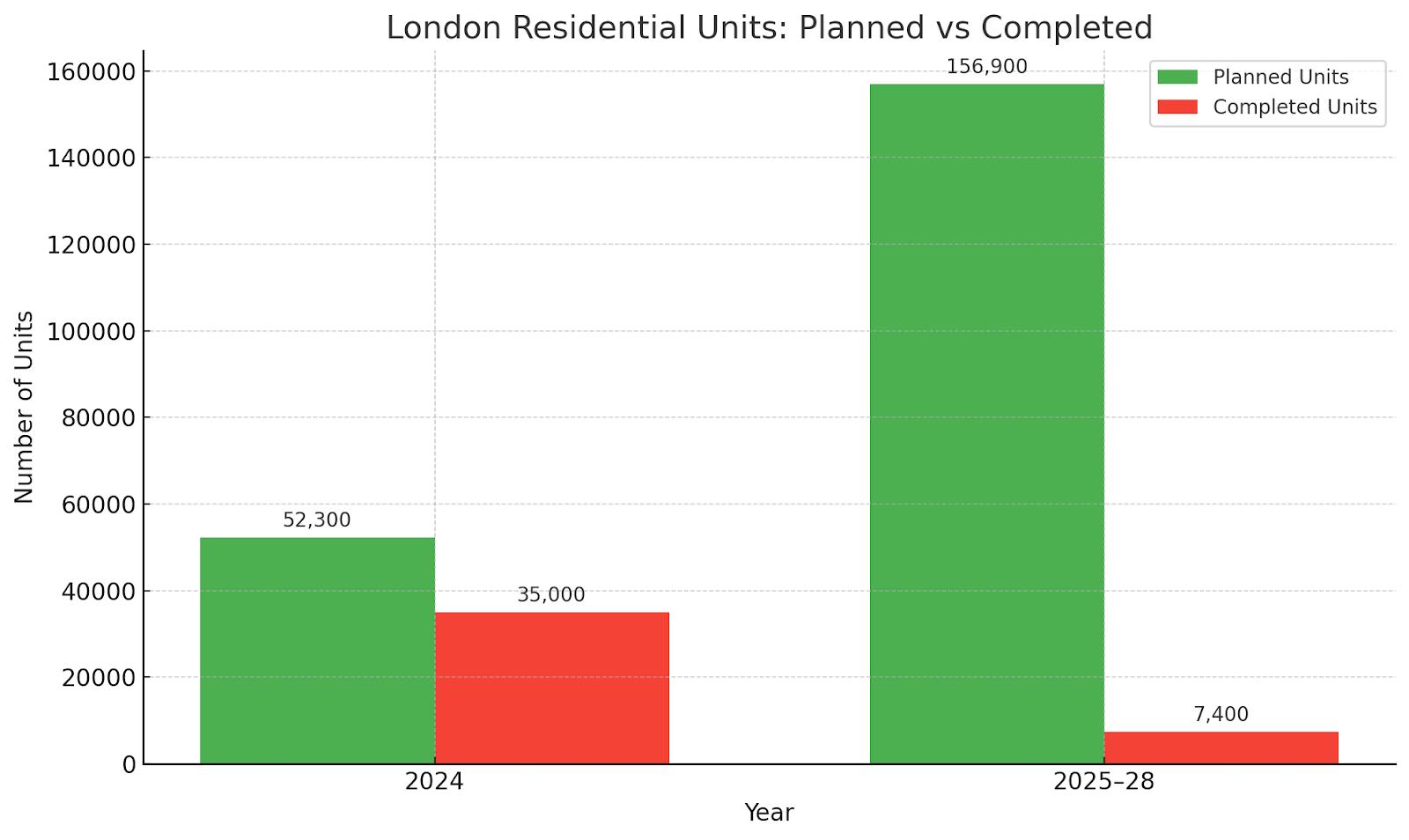

The city’s housing supply remains severely constrained. Greater London Authority (GLA) data shows only 1,210 private flats were started in Q1 2025, marking the lowest quarterly start since 2009. Meanwhile, total completions in 2024 dropped to 35,000 units, falling far short of the London Plan’s target of 52,300 homes per year.

Several structural barriers are to blame: prolonged planning timelines, high post-Brexit labour costs, and inflation-driven material prices. While planning submissions have ticked up slightly, the GLA forecasts only 7,400 units delivered by 2027–28, a fraction of what’s needed. This chronic undersupply is driving long-term pressure on affordability and investor confidence.

Demand Drivers: First-Time Buyers and Global Investors

Despite headwinds, demand for new build homes remains resilient. Knight Frank reports that 13% of transactions are led by international buyers, particularly from Asia and the Middle East, seeking EPC A/B-rated flats in well-connected zones. These buyers are drawn to energy efficiency, “chain-free” status, and the relative safety of London’s legal system.

First-time buyers are also regaining ground. After the Bank of England’s May 2025 rate cut to 4.25%, average two-year fixed mortgage rates dipped below 4%, according to Zoopla. Combined with government Help-to-Buy successors and rising rental costs, this has led to a 6% year-on-year increase in agreed sales among domestic buyers.

Innovation & Sustainability: PropTech and EPC Focus

Technology continues to transform the buying experience. AI-powered platforms like Entralon are helping buyers discover high-performance units across London, filtering by energy rating, location, and off-plan incentives in real time.

Sustainability is now a non-negotiable. Over 60% of new build units in Greater London now meet EPC A or B standards, qualifying them for green mortgage schemes and reduced utility bills. Developers are also responding to Part L of the UK Building Regulations, delivering homes with low carbon footprints, smart metering, and high thermal performance, especially in projects across Canary Wharf, Nine Elms, and King’s Cross.

Economic Challenges: Stamp Duty, Tariffs, and Rates

London’s macroeconomic landscape is mixed. While the BoE’s rate cut boosted mortgage affordability, the government’s reduction of the SDLT nil-rate threshold to £125,000 has made mid-range purchases more expensive. For instance, a buyer of a £425,000 home now pays £6,205 in stamp duty, up significantly from 2023.

On a larger scale, concerns over a potential US–UK tariff war, persistent inflation, and weak GDP growth (forecast at just 0.9% in 2025 by Pantheon Macroeconomics) are dampening investor confidence. However, speculation around a new UK–US trade agreement offers a potential mid-year boost to market sentiment.

Conclusion for Buyers and Investors:

London isn’t leading on growth in 2025, but it still leads in stability, transparency, and legal security. With rising interest in regeneration zones like Southbank, Barnsbury, and Holloway, plus strong performance in energy-efficient housing, the city continues to offer predictable long-term value in a volatile global landscape.

Looking to discover London’s best-performing off-plan and new build homes, filtered by price, EPC rating and regeneration potential?

Let Entralon empower your journey with verified listings, real-time data, and no-agent algorithms.

Dubai vs London Property Market 2025: Price Growth, Yields, Risk & Investor Insights

As 2025 unfolds, global investors are increasingly comparing London’s stability with Dubai’s rapid ascent, two powerhouse cities with fundamentally different market dynamics, regulatory frameworks, and investment narratives. This section offers a detailed, side-by-side analysis of how each performs across key indicators for property buyers and institutional investors.

Price Growth: Dubai Leads, London Trails

In terms of annual price performance, Dubai is far ahead. According to REIDIN, apartment prices surged by 19.4% year-on-year as of November 2024, driven by a wave of off-plan launches and strong foreign investor appetite.

London, in contrast, saw a 2% annual increase in Q3 2024 (Knight Frank), with temporary price dips recorded in early 2025, most notably a 0.8% monthly drop in June (Nationwide), largely due to stamp duty threshold cuts and affordability concerns.

Bottom line: Dubai offers strong short- to mid-term capital growth, while London provides long-term value with lower volatility.

Supply & Delivery: Dubai Builds, London Delays

Dubai’s supply pipeline is aggressive and well-funded. According to Cavendish Maxwell, 76,000 new units are expected in 2025, and over 243,000 by 2027, particularly in zones like Jumeirah Village Circle (JVC) and Dubai South.

By contrast, London faces structural undersupply. The Greater London Authority (GLA) reports just 1,210 private units started in Q1 2025, the lowest since 2009. And in 2024, only 35,000 completions were recorded, far short of the 52,300-unit target in the London Plan (CBRE).

Dubai may face oversupply risk, while London’s shortage keeps upward pressure on prices.

Buyer Profile & Incentives: Expat ROI vs. Local Entry Barriers

Dubai has positioned itself as a magnet for global investors and expats, offering:

- 7.6% + average rental yields

- 0% property tax

- Pathways to residency via the Golden Visa program

Buyers from India, China, the UK, and Russia dominate the off-plan segment, attracted by affordability, flexible payment structures, and fast delivery timelines.

London still appeals to international buyers (13%), but presents:

- Higher entry costs

- Stamp duty burdens (e.g., £6,205 on a £425,000 flat)

- Stricter legal and financial regulations

Average rental yields hover around 2.4%, though long-term appreciation and currency safety continue to attract institutions and wealth-preserving buyers.

Dubai favours ROI-seekers and entrepreneurs; London suits institutional or long-term, low-risk investors.

Sustainability & Innovation: Both Strong, But in Different Ways

Dubai leads in luxury-branded residences (140+ in pipeline) and green-certified construction. According to DAMAC, around 35% of all new builds are LEED-certified. High-end projects integrate:

- Smart metering

- AI-powered building systems

- Energy monitoring and optimisation

London, by contrast, is a PropTech pioneer. Platforms like Entralon provide AI-powered property discovery, EPC-based filtering, and price benchmarking. The city also leads in regulatory green standards:

- Over 60% of new builds achieve EPC A/B

- Most comply with UK Building Regulations Part L

- Common features include smart heating, thermal insulation, and net-zero design

Dubai shines in branded scale and innovation; London excels in performance, compliance, and buyer transparency.

Risk & Outlook: Dubai’s Acceleration vs. London’s Cautious Recovery

Dubai’s market is accelerating but with cautionary signals. With 59% of transactions off-plan (as of April 2025) and construction timelines tightening, risks of oversupply may materialise by late 2026. Meanwhile, broader Middle East tensions, though currently contained, remain variables for geopolitical risk.

London’s recovery is more measured. GDP growth is forecast at 0.9% (Pantheon Macroeconomics), and supply delays persist. However, London benefits from:

- Legal transparency

- Regulatory consistency

- Currency strength

These factors lower downside volatility and make it a safe-haven market in times of global uncertainty.

Dubai’s speed brings opportunity and exposure; London’s caution delivers predictability and regulatory insulation.

Final Thoughts

Whether you’re investing, relocating, or simply exploring your options, understanding the contrasts between Dubai and London can shape smarter decisions:

- Dubai is ideal for those seeking high rental yields, agile growth, and residency-linked opportunities. It’s a market built for momentum, off-plan flexibility, and global investor access.

- London offers a more measured path: long-term capital stability, ESG-aligned assets, and transparent regulation in one of the world’s most established property markets.

Still deciding between Dubai and London?

Let Entralon be your guide. Contact us.

FAQ

1. Is Dubai or London better for property investment in 2025?

Dubai offers higher rental yields and tax advantages, making it attractive for short- to mid-term investments. London provides long-term stability and strong legal protections, appealing to risk-averse investors seeking steady capital appreciation.

2. What are the average rental yields in Dubai and London in 2025?

As of 2025, Dubai’s average rental yields range between 5% and 9%, depending on the property type and location. In contrast, London’s rental yields average between 2% and 4%, with variations across different boroughs.

3. Are there property taxes in Dubai?

No, Dubai does not impose annual property taxes, capital gains tax, or income tax on rental income. This tax-free environment enhances the net returns for property investors.

4. Can foreigners buy property in Dubai and London?

Yes, foreigners can purchase property in both cities. In Dubai, non-residents can buy freehold properties in designated areas with full ownership rights. In London, there are no restrictions on foreign property ownership, though buyers may be subject to certain taxes and regulations.

5. What is the outlook for property prices in Dubai and London in 2025?

Dubai’s property market is expected to maintain its upward momentum, driven by strong demand and investor-friendly policies. London anticipates modest but stable growth, supported by improved mortgage conditions and a strong legal framework.

Discussion