Beyond the Headlines: What’s Driving the UK Housing Conversation

Everyone seems to be talking about buying in London. From social media influencers showcasing slick off-plan penthouses to friends debating whether now is the “right time” to buy, the UK property market, especially in London, remains a global fixation. But behind the glossy marketing and market summaries lies a much more complex story: one shaped by policy gaps, structural demand shifts, regional divergence, and evolving investor appetites.

In 2024, the UK government reasserted its commitment to delivering 1.5 million new homes in England by 2030. Yet despite this bold policy target, recent data shows that housing delivery remains consistently below the required pace. Meanwhile, even in the face of limited supply, overall transactions are falling, mortgage accessibility remains tight, and affordability continues to constrain both end-users and developers.

For global investors, digital-first buyers, and those exploring property as a route to residency or long-term returns, the UK market, particularly beyond the usual London headlines, offers both risks and opportunities. But to unlock them, one must first understand the forces currently reshaping the housing ecosystem in 2025.

Want to go beyond the headlines?

Explore verified off-plan and new-build properties in London on Entralon.

Why Supply Alone Can’t Revive UK Housing Delivery?

Understanding the Demand-Side Block in UK Housing (2025)

In theory, a limited housing supply should push up transactions. But in today’s UK housing landscape, demand-side constraints are proving just as severe, if not more so, than supply issues.

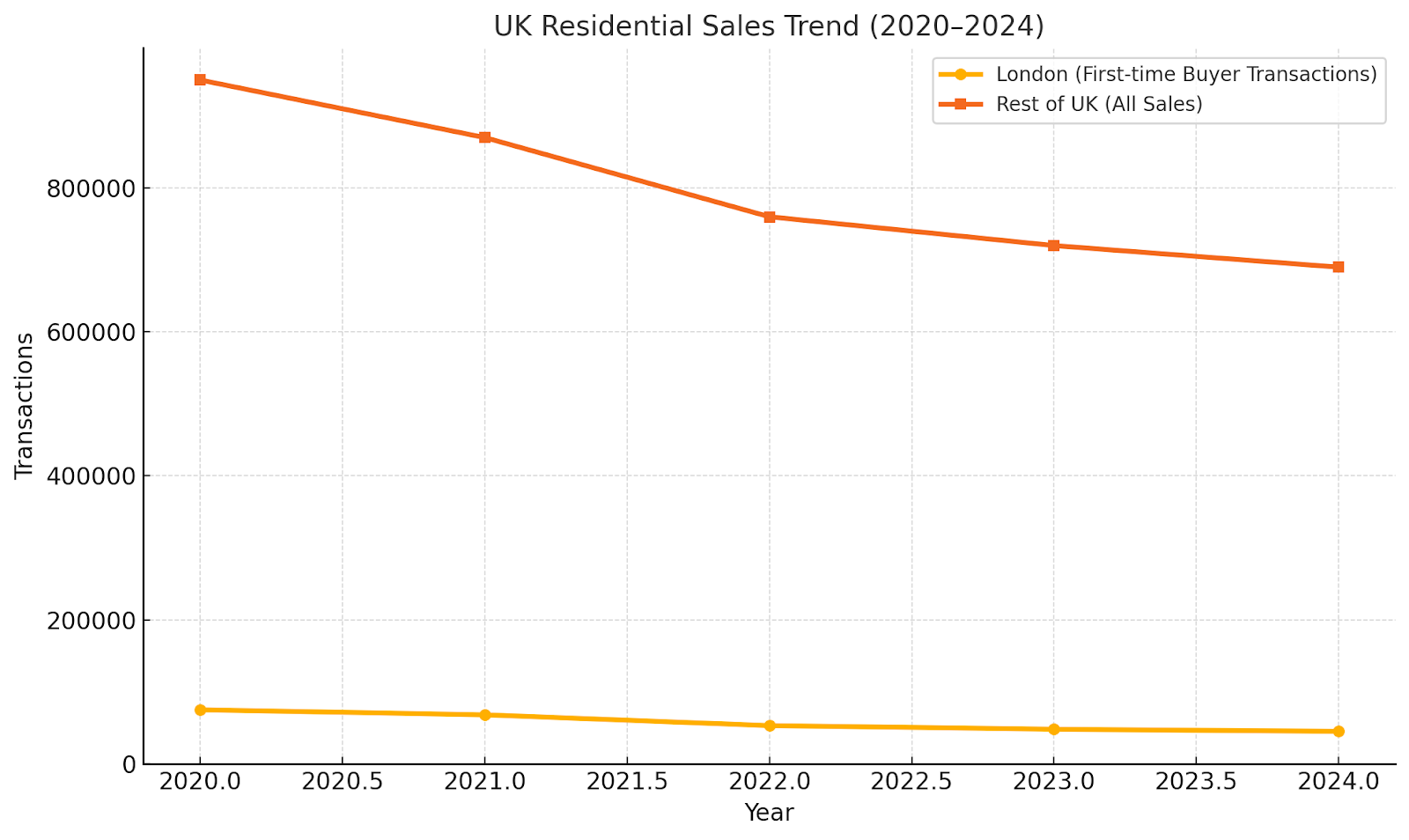

Over the past two years, new housing completions have remained below the government’s 300,000-per-year target. Even more telling is the sharp decline in transactions: total residential sales dropped by over 26% between 2022 and 2024, according to HM Land Registry. This points to more than a developer-side bottleneck; it reflects a broad erosion of purchasing power across the market.

Affordability Barriers, Not Just Supply Shortages

High inflation, successive interest rate hikes, and stagnant wage growth have created a triple-layered affordability constraint. Between early 2021 and mid-2024, average mortgage rates surged from 2.1% to 5.8%, significantly reducing loan capacity, especially for first-time buyers.

Many households that qualified for mortgages just a few years ago now face rejections or unsustainable monthly payments. Stricter loan-to-income (LTI) limits and affordability stress tests further restrict access, shrinking the buyer pool, particularly in high-ratio regions such as London, Oxfordshire, and the South East.

The Transaction-to-New-Build Ratio Confirms the Slowdown

The well-established 10-to-1 ratio, indicating that one new build typically starts for every ten housing transactions, shows how tightly delivery is linked to market activity. With transactions falling sharply, new-build output has declined in parallel. This isn’t due to a lack of planning permissions, but rather to limited sales absorption and weak buyer confidence.

Rental Growth Alone Can’t Offset Demand Weakness

While owner-occupier activity has slowed, the private rental sector, particularly Build-to-Rent, is expanding. However, this growth, largely driven by institutional capital, serves different segments and pricing tiers. It cannot replace the demand shortfall among first-time buyers or traditional home-seekers.

Demand-Side Reform Is Essential

The UK housing market is caught in a feedback cycle: weakened demand suppresses supply, and constrained supply keeps prices elevated. Without coordinated policy interventions, such as mortgage reform, inflation control, and renewed buyer incentives, construction alone will not restore delivery momentum.

Regional Trends and Investment Opportunities: London, Midlands, and the North

While UK-wide averages paint a story of stagnation, regional housing markets reveal a far more nuanced reality, one where challenges coexist with strategic investment opportunities. Understanding these shifts is essential not only for institutional players but also for international buyers, tokenised investors, and those seeking long-term residency through property acquisition.

London: Global Demand Meets Local Inaccessibility

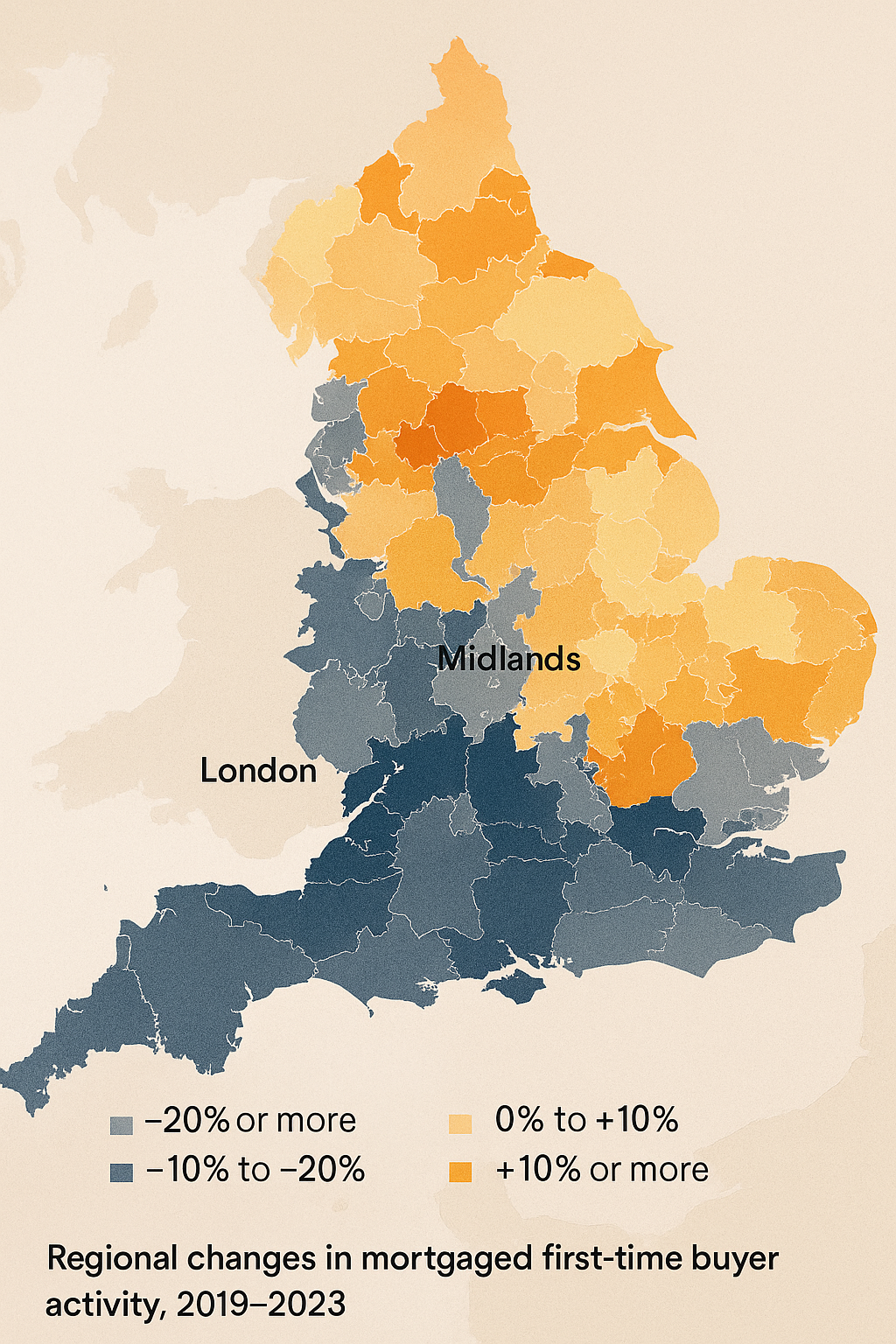

London continues to attract global attention, but remains deeply polarised by affordability. Despite its role as a global financial and cultural hub, affordability barriers and tight mortgage criteria have pushed first-time buyer activity to historic lows. ONS data shows that between 2019 and 2023, multiple boroughs, such as Westminster, Camden, and Newham, experienced over 15% drops in mortgage transactions.

Yet within this challenge lies a unique investment window. As transaction volumes have cooled, price growth has stabilised, particularly in regeneration zones like Acton, Barking, Woolwich, and Croydon. Crossrail connectivity and local infrastructure upgrades are making these submarkets more attractive, offering a rare blend of urban access, relative affordability, and potential capital appreciation over a 5–7 year horizon.

Curious where these hidden gems lie?

Explore our guide to London areas where first-time buyers can still purchase homes under £600,000, backed by transport links, community value, and long-term potential.

Midlands: Resilient Fundamentals and Urban Regeneration

The Midlands, especially Birmingham, Coventry, and Leicester, presents a different narrative. These cities benefit from regeneration projects like Paradise in Birmingham, improved transport links including HS2, and high graduate retention from regional universities. While national housing transactions dropped 26% since 2022, key Midlands cities saw declines of only 8–10%, indicating stronger market resilience.

Birmingham’s Build-to-Rent sector is flourishing with institutional funding, and suburban areas like Solihull, Dudley, and Walsall report rental yields between 5.5–6.2%, paired with entry-level home prices below £230,000. These fundamentals position the Midlands as a prime zone for both long-term renters and first-time property investors.

Northern England: Affordability, Incentives, and Quiet Momentum

Northern cities such as Manchester, Leeds, and Newcastle are quietly reshaping the dynamics of UK housing delivery. Manchester now leads the country in forward-funded BTR projects, while Sheffield and Liverpool maintain average gross yields of 6.5–7.2%, among the highest nationwide.

Local authorities in Bradford and Hull are actively rolling out developer incentives and urban renewal schemes, supporting both investors and owner-occupiers. With average home prices in many parts of the North still under £200,000, these cities offer unmatched affordability, particularly for international buyers seeking hybrid use (residency + income).

Strategic Insight: The UK’s housing opportunity is no longer a London-only story. From high-growth rental yields in northern cities to regeneration-led appreciation in Midlands hubs, regional diversification is not just a risk hedge; it’s an intelligent entry strategy.

Mortgage Policy, Affordability, and the Future of Lending: What’s Holding Back the Real Buyer Base

The Structural Barrier Behind Demand Weakness

For many aspiring homeowners, especially first-time buyers, international investors, and those pursuing UK residency through property, the primary obstacle is no longer the lack of homes. It’s affordability and access to mortgage finance. Post-2008 lending reforms may have stabilised the system, but they now act as a structural constraint on housing delivery.

The Rise of the Affordability Wall

Since 2014, the Mortgage Market Review (MMR) has enforced strict affordability checks. Banks must “stress-test” whether buyers can still afford repayments under hypothetically higher interest rates. Combined with loan-to-income (LTI) caps, this system blocks many households with stable incomes, especially in high-cost areas, from obtaining mortgages.

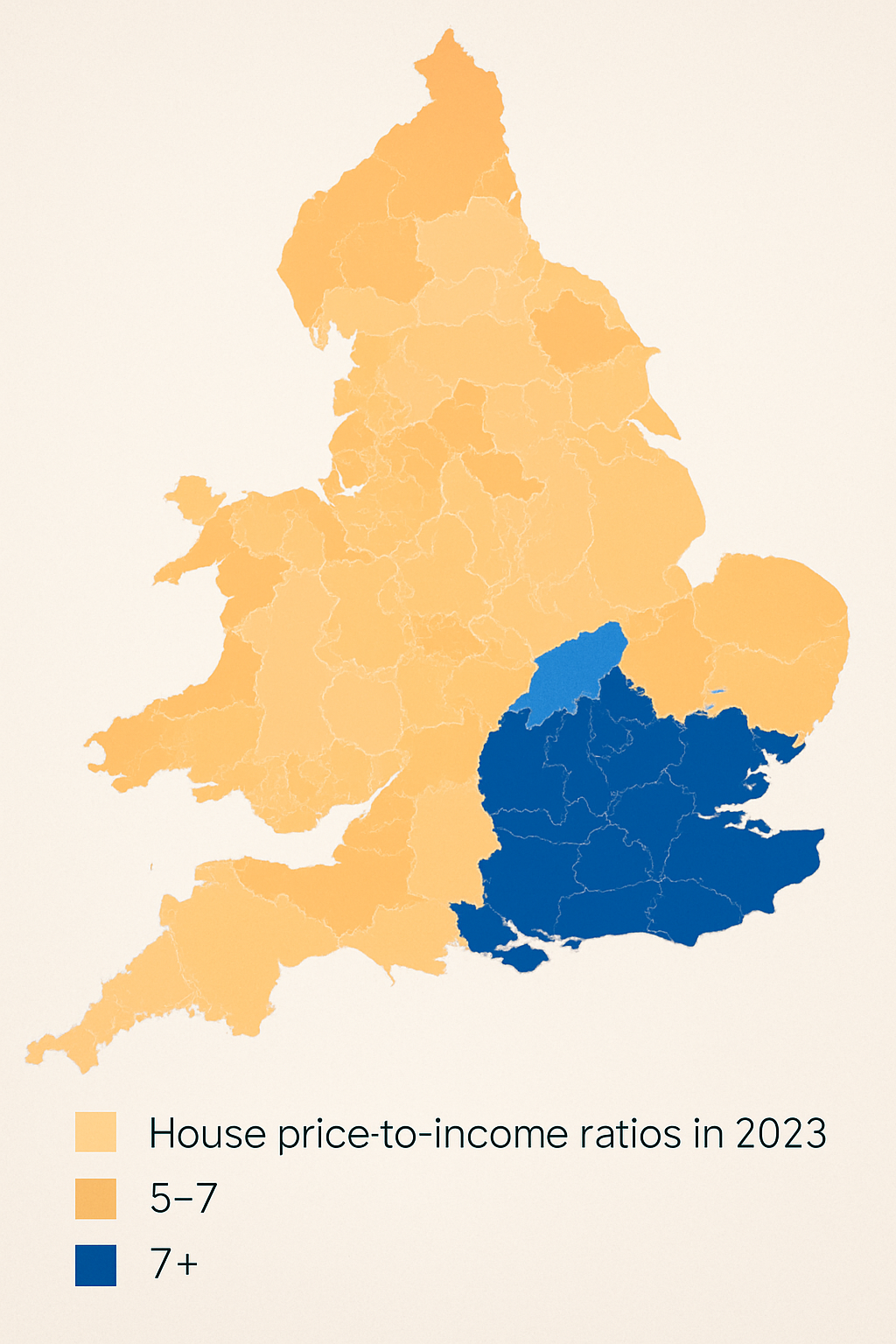

In London and the South East, where average prices exceed £500,000, this becomes critical. According to the ONS, London’s price-to-income ratio hit 12.5 in 2023, compared to 6.8 in the Midlands and 5.3 in the North. These figures make market entry nearly impossible without significant policy or financial support.

Even households with sufficient income to cover monthly repayments are being excluded due to high deposit demands or “failing” affordability stress tests.

The End of Help to Buy and the Missing Link

Between 2013 and 2023, the Help to Buy equity loan scheme addressed this affordability gap for over 50,000 households annually. It reduced deposit requirements and was tied specifically to new-build homes, offering both buyer confidence and builder incentives.

Its closure has left a void. While regional schemes like First Homes and Shared Ownership exist, they often:

- Lack of national reach,

- Include eligibility caveats (such as income limits or local authority restrictions),

- Face challenges around transparency and resale conditions.

Meanwhile, private lenders remain cautious in a volatile interest rate environment, further constraining mortgage access.

Regulatory Review: Is Change on the Horizon?

In 2024, the Financial Conduct Authority (FCA) launched a consultation on revising core lending rules. Key proposals include:

- Extending maximum mortgage terms to 35–40 years,

- Adjusting stress test assumptions to reflect post-pandemic conditions,

- Introducing targeted flexibility for first-time buyers and new-build transactions.

However, experts argue these proposals do not go far enough. These are technical adjustments, not structural reforms. Unlike Help to Buy, which directly changed the economics of entry, these updates do not reduce deposits or expand the qualified buyer pool. They remain regulatory, not fiscal.

Investor Impact and Broader Market Effects

This tightening affects more than end-users. For institutional and tokenised investors, a shrinking buyer base means:

- Lower exit liquidity,

- Slower capital turnover,

- Greater exposure to rental dependency.

Foreign investors seeking hybrid use (residency + capital growth) may face delays in ownership conversion or limitations on resale. Over-reliance on non-local capital, particularly in regeneration zones, creates fragile ecosystems that are vulnerable to policy shifts and tax changes.

Strategic Insight: The UK’s housing delivery targets are unlikely to be met unless mortgage policy evolves. Without a renewed fiscal support scheme or innovative lending mechanisms, homeownership will remain out of reach for millions, and developers will remain hesitant to build.

Institutional Capital and the Rental Revolution: Build-to-Rent and the Rise of Multifamily Housing

As homeownership remains elusive for many across major UK cities, especially London, Manchester, and Birmingham, the rental sector is entering a new era. This transformation is led by institutional investors, powered by Build-to-Rent (BTR), and shaped by the emerging multifamily model. These shifts represent not only a new delivery mechanism but a transformative investment strategy for the decade ahead.

From Buy-to-Let to Build-to-Rent: A Structural Shift

For years, the UK’s private rental sector was dominated by individual landlords operating under the traditional buy-to-let (BTL) model. But tax reforms, regulatory tightening, and economic volatility have made small-scale landlording increasingly unattractive.

Institutional capital has stepped in with a different vision and lasting impact.

From 2022 to 2024, the UK BTR sector attracted over £14 billion in investment, according to Savills. Projections suggest another £23 billion is expected by 2027, much of it directed at forward-funded developments rather than existing stock.

The rationale is clear:

- Professional property management,

- Predictable, lease-backed income streams,

- Consistent tenant demand from households priced out of ownership.

These investments aren’t just passive plays; they are actively reshaping how housing is built, delivered, and experienced. For instance, Greystar and Legal & General are pioneering large-scale multifamily developments with amenities like co-working lounges, on-site gyms, and integrated tenancy platforms.

Multifamily in the UK: From Trend to Core Strategy

The term “multifamily housing”, long established in the U.S., refers to residential buildings built specifically for long-term rental and managed professionally. In the UK, this model is rapidly becoming mainstream.

According to the 2025 European Living Survey, 63% of UK institutional investors now prioritise multifamily development. Why?

- Urbanisation and delayed homeownership create stable demand;

- Renters increasingly prefer buildings with shared spaces and digital services;

- Investors benefit from portfolio diversification and inflation-hedged yields.

Cities like Manchester, Birmingham, and Leeds are emerging as multifamily hotspots, offering:

- High renter demand,

- Strong planning support,

- Yields ranging between 4.5–6% often above national averages.

Strategic Advantage: Liquidity, Stability, and Policy Alignment

In today’s uncertain macroeconomic environment, BTR and multifamily assets offer a rare combination of:

- Income stability through lease-backed flows,

- Liquidity via REITs and emerging fractional ownership platforms,

- Strong alignment with government goals to professionalise the private rental sector (PRS).

Notably, 75–85% of recent institutional housing capital has gone into new construction, directly supporting housing supply and economic activity. These developments also play a counter-cyclical role, sustaining delivery pipelines even during private market downturns.

Key Challenges: Planning, Regulation, and Tenant Protections

Despite momentum, the BTR sector still faces headwinds:

- Planning systems often lack tailored frameworks for large-scale rental schemes.

- Uncertainty around rent control or tenancy reform may delay investor decisions.

- Quality standards and community integration vary across projects.

To unlock full potential, the UK government must:

- Provide clear BTR-specific planning guidance,

- Offer predictable regulatory frameworks,

- Support balanced tenant protections that do not erode investor confidence.

Why Build-to-Rent Is the Fastest-Growing Housing Model in the UK

BTR and multifamily are more than market trends; they are strategic responses to a changing demographic and financial reality. With professional operation, scalable delivery, and long-term financial resilience, they are fast becoming the foundation of a resilient, long-term housing strategy in the UK.

Thinking of buying for rental income in London?

Explore Entralon’s full-market view of new-build properties,

No hidden listings, no developer bias.

Then let our data-driven advisory team help you identify the most resilient, tenant-ready investment zones.

The Rise of Retail Investment: Why Mid-2025 Offers a Strategic Window

As institutional investors continue to shape the UK property landscape, mid-2025 presents a distinct opportunity for individual and first-time investors. This section explores why current conditions offer a strategic entry point and how Entralon enables transparent, data-informed decisions without commission bias.

A Market Ripe for Strategic Entry

While institutional capital dominates industry headlines, private investors are entering a moment of rare market equilibrium. Following a period of price stabilisation, regulatory recalibration, and evolving mortgage criteria, 2025 presents one of the most balanced conditions in years, especially for those targeting long-term value and residency potential.

Key indicators:

- Stabilised prices in regeneration zones across London, Birmingham, and Leeds

- Rental yields of 5–6% in selected northern and Midlands postcodes

- Loosening of mortgage restrictions is currently under review by the FCA

Together, these conditions create a compelling window, before the next upward price cycle, but with less pressure than in post-pandemic peaks.

Limitations of Traditional Property Platforms

Most platforms primarily serve developers, not buyers.

Commission-led incentives distort listings, prioritising promotional content over transparent comparison. For international buyers, particularly from the Middle East or Europe, this creates additional friction: complex regulations, inconsistent terminology, and a lack of clarity around rentability, resale potential, or location viability.

The Entralon Approach: Data-Driven, Neutral, Global

Entralon operates not as a listing platform, but as a buyer-aligned intelligence layer. Whether you’re based in London, Dubai, or abroad, we remove commission-driven bias and provide verified, structured property data.

Entralon aligns every opportunity with your financial, lifestyle, and visa objectives through a framework built on transparency and trust.

Contact Entralon.

Final Thoughts

For years, access to the UK housing market, particularly in London, remained out of reach for many. Escalating prices, fragmented regulation, and limited financing options left buyers navigating between unaffordable ownership and short-term rental alternatives. But 2025 marks a shift.

Today, the alignment of policy review, regional price adjustments, and innovation in housing finance has opened a strategic window, not just for institutional players but for individual buyers seeking long-term stability, rental yield, or visa pathways through property ownership.

Whether you’re evaluating full ownership or seeking fractional entry, Entralon helps you navigate with transparency, not pressure.

FAQ

1. Why are UK property sales low despite high demand and limited supply?

UK property sales remain low because of strict mortgage affordability rules, high deposit requirements, and the end of key support schemes like Help to Buy. Even qualified buyers often fail stress tests or can’t meet loan-to-income caps, especially in high-cost regions.

2. Which UK regions offer the best real estate investment opportunities in 2025?

In 2025, the Midlands, Northern cities like Manchester and Leeds, and emerging London submarkets such as Barking and Woolwich offer the strongest investment prospects due to regeneration projects, strong rental yields, and relative affordability.

3. What is Build-to-Rent (BTR) and why is it growing in the UK?

Build-to-Rent (BTR) is a housing model where entire residential developments are built for long-term rental and managed professionally. It’s growing in the UK because of rising demand from renters, institutional investor interest, and alignment with government policy to expand high-quality rental housing.

4. Is 2025 a good time to invest in UK real estate?

Yes, 2025 offers a rare window of opportunity due to policy reforms, recalibrated pricing, and innovation in housing finance. Regional markets like the Midlands and the North are especially attractive for investors seeking growth and value.

5. What makes Entralon different from other property platforms?

Entralon offers an unbiased, data-driven approach with zero commission bias. It showcases every new-build and off-plan project in London and Dubai, provides personalised guidance, and doesn’t accept marketing fees from developers, ensuring transparency and buyer-focused advice.

Discussion