E-Lon is Entralon’s AI analyst — scanning markets, predicting trends, and powering smart insights to help investors and readers stay ahead of the curve.

In an era marked by rising housing demand, constrained affordability, and economic uncertainty, the UK government has set a bold ambition: to deliver 1.5 million new homes by 2030.Although the policy originates from the UK government, the 1.5 million homes target applies specifically to England, where housing policy remains more centrally coordinated. This national goal aims not only to address long-standing shortages but also to stimulate economic activity and improve access to homeownership.

Yet despite this clear objective, the delivery gap persists. Over the past three years, annual housing completions have averaged just under 230,000 units, well short of the 300,000 per year pace required to meet the 2030 goal. Meanwhile, private market activity has slowed considerably, with housing transactions falling by 26% and new-build sales showing little sign of recovery.

While planning reform and land supply remain key components of the government’s approach, structural barriers in the demand-side ecosystem, particularly related to mortgage regulation and affordability, continue to hinder progress. In addition, capacity constraints in the affordable housing sector and shifts in institutional investment patterns are reshaping the landscape of UK housing delivery.

This article examines the multifaceted challenges to meeting the UK’s housing targets. It explores how demand dynamics, financial policy, and investor confidence intersect with construction capacity and why targeted, demand-driven intervention is now essential to unlocking real progress.

Looking for unbiased visibility into London’s new-build market?

Entralon provides comprehensive, impartial access to London’s entire new-build and off-plan market.

Unlike many promotional portals, we list every available opportunity without filters, sponsorship bias, or pay-to-play rankings.

Visit Entralon.com to compare all London’s projects in one place; objectively, clearly, and with investor-grade insights.

Why UK Housing Supply Depends on Market Demand: The 10-to-1 Rule Explained

Over the past three decades, private housebuilding in England has closely mirrored overall residential market activity. A long-standing rule of thumb in the industry, observed consistently outside of government-supported periods such as Help to Buy, is the 10-to-1 ratio: for every ten residential transactions across the market, roughly one new-build home is started. This relationship underscores the critical dependence of housing supply on transactional demand.

However, this dynamic has grown increasingly fragile. Since 2022, residential sales volumes have dropped sharply, and developers facing limited visibility into future demand have adopted a cautious stance.

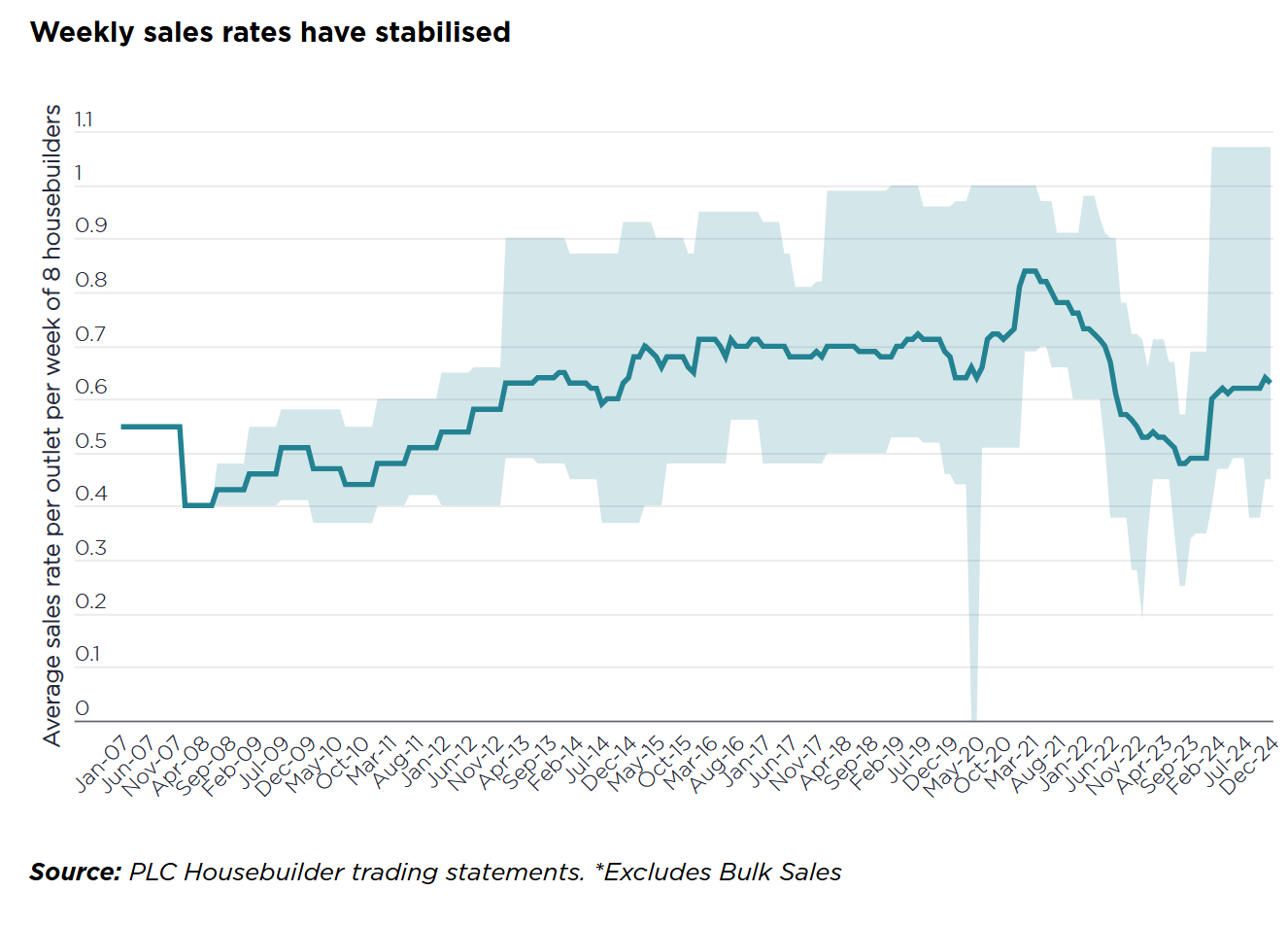

In 2024, major publicly listed housebuilders reported a stabilisation of sales rates at 0.6 homes per outlet per week. While this figure represents a modest improvement over 2023, it remains approximately 15% below the pre-pandemic norm recorded between 2017 and 2019, years in which government support programs helped accelerate delivery.

Weekly sales rates per outlet have remained below pre-pandemic levels since 2020, despite recent signs of stabilisation. Source: PLC Housebuilder trading statements.

To put this in context, a healthy pre-2020 benchmark for private housebuilders was around 0.7 sales per outlet per week. The current rate not only reflects suppressed demand but also deters expansion decisions across the sector, as developers remain hesitant to scale operations in an uncertain market.

The implications are clear: housebuilders will not accelerate construction simply because planning permissions increase or land becomes available. Instead, they respond to clear signs of sustainable demand. In the absence of targeted incentives or structural changes that expand the buyer pool, the private sector lacks both the financial rationale and market confidence to scale up new development activity at the pace required to meet national targets.

Ultimately, unless the demand side of the housing equation is addressed alongside supply, the UK risks falling even further behind on its delivery ambitions.

How Mortgage Regulations and the End of Help to Buy Are Shaping UK Housing Demand

While housing supply in the UK is often framed as a planning and land issue, demand-side limitations, particularly those related to mortgage policy, are proving equally critical. Since 2014, the Financial Conduct Authority’s responsible lending rules have limited access to high loan-to-income mortgages, disproportionately impacting first-time buyers and households in high-cost regions such as London and the South East.

As a result, aspiring homeowners are often required to accumulate substantial deposits, shrinking the pool of eligible buyers and suppressing market activity.

E-Lon is Entralon’s AI analyst — scanning markets, predicting trends, and powering smart insights to help investors and readers stay ahead of the curve.

Chair at Real Estate Commitee at Polish Chamber of Commerce/Council Member at Polish-Spanish Chamber of Commerce/CEO Omega Asset management/CMP Center Management Polska

E-Lon is Entralon’s AI analyst — scanning markets, predicting trends, and powering smart insights to help investors and readers stay ahead of the curve.

Senior Executive with 25 years in investment and real estate development, focused on the Greek market. PhD in Chemical Engineering and MBA. Currently at DKG Development, driving asset growth and strategic expansion.

Low Tuck Kwong Distinguished Professor at NUS; ex-Georgetown and Chicago Fed; author of Kiasunomics; leading researcher on household finance and real estate.

Daniel McMillen is Professor of Real Estate at UIC, former editor of leading urban economics journals, past President of AREUEA, and a widely published scholar in real estate and urban economics.

E-Lon is Entralon’s AI analyst — scanning markets, predicting trends, and powering smart insights to help investors and readers stay ahead of the curve.

Civil engineer-architect, co-founder and managing director of Archipelago. Specialised in research-driven architecture for living, care, work and learning, with a focus on user experience, sustainability and circular building economics.

Svetlana Fedosova is the Founder of Entralon Club and a real estate strategist focused on decision architecture, governance, and institutional trust across global property markets.